Can I Use My US Dental Insurance or HSA for Implants in Turkey?

Dr. Emrah YEŞİLYURT

Dr. Emrah Yeşilyurt is the Founder of Avangart Clinic. He combines advanced dental expertise with a genuine commitment to helping patients feel comfortable and informed about their oral health journey.

If you have been quoted a very high price for restorative dental work in the United States, it is natural to wonder whether you can use your existing health funds to help pay for treatment abroad.

Many patients looking at All-on-4 Dental Implants in Turkey are not trying to work around the system. They just want a clear answer on whether using US health funds overseas is legal, and whether the savings are real once everything is accounted for.

The answer begins with an important distinction. Standard US dental insurance usually offers little to no meaningful help for planned implant treatment outside the country, especially when the provider is outside the insurer’s network.

HSA (Health Savings Account) and FSA (Flexible Spending Account) funds work differently from standard dental insurance. The IRS focuses on the type of expense, not just where the treatment happens. If the dental care qualifies as an eligible medical expense, those rules can also apply to treatment received outside the United States.

That distinction matters for patients comparing implant costs in Turkey with the prices they have already been quoted in the United States. When pre-tax healthcare dollars are used correctly, the cost of care can become much easier to manage. That can apply to a single missing tooth, a more complex full-arch case, or implant surgery at a certified Turkish clinic where the treatment is clearly restorative rather than cosmetic.

Many patients miss this at the start: even if the treatment is legally eligible, that does not guarantee a smooth payment or reimbursement process. Your account administrator may still review how the treatment was documented, whether the procedure qualifies under your plan, and whether the records clearly show medical need. On top of that, overseas card payments can trigger foreign conversion fees, and some transactions are declined because of the way the clinic is coded in the payment system, not because the treatment itself is ineligible.

Does US Dental Insurance Cover Dental Work in Turkey?

For most patients, the answer is no. A standard US dental insurance card usually will not work in Istanbul the way it does with a domestic provider, because these policies are built around US networks, domestic billing rules, and pricing structures the insurer can verify.

That often leaves patients paying upfront, even when they still have active coverage at home. Once they compare their annual maximum, co-pay, waiting periods, and exclusions with the total cost of treatment abroad, many find that Turkey remains the more workable option for a major restorative case.

Why Standard PPO and HMO Networks Stop at the Border

HMOs are the most restrictive. They generally require pre-authorized treatment within a defined network, so they offer no practical path for planned dental tourism or a complex case such as all-on-6 treatment in Turkey.

PPO plans give patients more flexibility, but that flexibility is still usually domestic. “Out of network” rarely means “any licensed clinic anywhere in the world.” It usually means a US provider outside the insurer’s preferred network, with reimbursement still tied to domestic claim systems and domestic fee benchmarks. Some plans may help with true emergencies abroad, but that is very different from pre-planned implant treatment.

This is where many patients run into problems. Travel-related dental benefits, when they exist, are commonly limited to urgent care such as pain relief or emergency treatment, not elective restorative oral surgery booked in advance. Multi-unit implant cases, full-arch reconstruction, and a staged dental implant procedure usually fall outside those limited travel benefits.

Annual maximums are another limitation. Many US dental plans still place a relatively low cap on how much they will pay in a year, and that amount can be used up quickly in implant cases.

Even one implant may absorb a large share of the available benefit, leaving the patient responsible for the rest of the treatment cost.

Premium Out-of-Network Allowances: The Rare Reimbursement Exception

A small number of premium executive PPO or international indemnity plans can reimburse care received abroad, but this is the exception, not the rule. Before traveling, the patient needs written confirmation of international benefits, the claim pathway, the foreign fee schedule if one applies, and how the insurer calculates Usual, Customary, and Reasonable rates.

Even then, reimbursement often happens after treatment, not before. That means paying upfront, then filing a retrospective claim with itemized receipts, diagnostic records, and sometimes translated documents. The insurer may reimburse only a limited amount based on its internal UCR formula, which can leave a large unpaid balance. At that point, many patients move to a more practical question: is dental treatment in Turkey a safe and workable option when HSA or FSA funds may offer a more reliable payment route?

Can You Use an HSA or FSA for Dental Care Abroad?

Yes, often you can. Many US patients assume an HSA or FSA only works inside the United States, but that is not how the tax rules work. The IRS looks at the type of treatment first. If the expense is a valid medical or dental cost, the fact that your care takes place in Turkey does not automatically disqualify it.

This is why dental treatment abroad can still fit within US tax rules. The main question is whether the procedure counts as a qualified medical expense. The second question is whether your account provider or plan administrator will ask for additional documentation before approving the payment or reimbursement.

The IRS Rulebook: Validating International Qualified Medical Expenses

Under the official guidelines of IRS Publication 502, eligible medical and dental expenses can include the costs of diagnosing, treating, easing, or preventing disease, as well as care that affects the structure or function of the body. Dental treatment can fall under that rule when it restores health and function. The IRS does not limit that rule to one country.

That gives patients a clearer legal basis for using those funds. If your treatment in Turkey would qualify as necessary dental care under US tax rules, it may still qualify when performed abroad. The care must also be lawful in the country where it is provided, and your records should clearly explain why the treatment was medically necessary.

Restorative vs. Cosmetic: The Fine Line Governing Implants and Veneers

This is where the details matter. Dental implants are usually considered restorative treatment, not cosmetic treatment. A titanium dental implant fixture replaces a missing tooth root, supports the crown above it, and helps restore biting and chewing. When a patient has tooth loss, the implant is there to replace lost structure and improve function.

The same logic often applies to related procedures such as bone grafting, sinus lift surgery, abutments, and implant-supported crowns. These are part of rebuilding the mouth after missing teeth, dental trauma, or advanced decay. In tax terms, that places them much closer to medical care than optional appearance work.

Cosmetic treatment is treated differently. Whitening, smile enhancement done only for looks, or veneers placed only to change appearance are usually not eligible. Veneers may be easier to justify only when they repair real structural damage, such as trauma, severe decay, or a developmental defect documented by a dentist.

Legal Mechanisms for Deploying HSA and FSA Funds in Turkey

Using HSA or FSA money in Turkey is usually less about legal eligibility and more about payment method. Many patients assume the easiest path is to swipe their benefit card at the clinic. In reality, the smoother path is often to pay first with a regular bank card and then handle reimbursement through the US account system.

The Debit Card Processing Trap: Why Swiping Often Fails Overseas

An HSA or FSA card may carry a Visa or Mastercard logo, but that does not guarantee it will work abroad. Many account administrators use automated fraud filters, country controls, and merchant screening rules. If the foreign Merchant Category Code (MCC) or transaction pattern does not fit the system, the payment may be declined even when the dental expense itself is eligible.

That can cause problems when it is time to pay. We have seen patients prepare well for treatment, then run into card problems because they relied on one payment route. A foreign transaction or currency conversion fee may also apply, which adds extra costs the patient did not expect. HealthEquity, for example, notes a 1% to 3% overseas fee on eligible card use.

For that reason, it is safer to keep a primary backup payment method ready. A standard credit card or bank debit card gives you more control if the benefit card fails.

The Reimbursement Framework: Safeguarding Your Tax-Advantaged Capital

For many US patients, reimbursement is the more reliable option. You pay the clinic directly, keep your records, and then recover the funds through your HSA or FSA. This avoids a point-of-sale rejection in Turkey and lets you manage the paperwork on your own timeline.

With an HSA, the account holder usually pays for the treatment and then keeps records showing that the money was used for a qualified medical expense. The IRS places the recordkeeping duty on the patient. That means saving invoices, treatment records, proof of payment, and any notes that explain medical need.

With an FSA, reimbursement usually goes through the plan administrator first. Before any money is returned, the claim may need itemized documents and formal approval. Good records make that process much easier, especially when the treatment was received outside the United States.

Administrative Documentation Required by US Account Administrators

When you use HSA or FSA funds for treatment in Turkey, the burden of proof sits with you. US account administrators and the IRS expect you to show that the money went to a qualified medical expense, not a cosmetic service. That is why it is smart to ask for the right paperwork before you leave the clinic, not after you get home.

A basic receipt is rarely enough. For most claims, you should keep:

- An itemized invoice that lists each treatment separately

- A clinical summary or formal diagnosis

- Proof of payment showing the amount, date, and payment method

- Imaging files, radiographs, or treatment notes where relevant

- An English translation if the original documents are not clear enough for review

Designing a Bulletproof Letter of Medical Necessity (LMN)

A Letter of Medical Necessity (LMN) can strengthen an implant claim when the treatment might otherwise be mistaken for cosmetic work. For a US benefits administrator, the strength of the letter often comes down to one thing: whether it clearly shows that the treatment addresses a real clinical problem affecting oral health and function.

The letter should come from a licensed dental practitioner and use formal diagnostic language rather than broad consumer wording. It should identify the patient’s condition in clear clinical terms, such as partial edentulism, advanced alveolar ridge resorption, non-restorable tooth fracture, severe structural tooth loss, compromised occlusal function, or masticatory dysfunction. Those details help frame the case as restorative care tied to chewing, stability, and the preservation of oral structures.

A strong LMN should also connect the diagnosis directly to the proposed treatment. It is not enough to list “implant treatment” on its own. The letter should explain why the implant fixture, bone graft, abutment, crown, or implant-supported prosthesis is medically necessary for that patient, what function it restores, and what problem it is intended to correct. If the patient has difficulty chewing, bone loss after missing teeth, failure of an existing restoration, or a fractured tooth that cannot be saved, the letter should state that clearly.

For the best chance of standing up to review later, the LMN should include:

- The patient’s full name and date of birth

- The clinician’s name, credentials, and signature

- The formal diagnosis

- The recommended treatment plan

- The clinical reason that treatment is necessary

- The expected treatment timeline

- Reference to supporting records such as radiographs, CBCT findings, photographs, or chart notes

In implant cases, the most persuasive LMNs read like a clinical pathway rather than a brief note of support. They show what condition exists, how it affects daily oral function, why the proposed treatment is needed, and how the records support that recommendation. That kind of documentation gives an FSA or HSA reviewer a much clearer basis for approving a legitimate restorative claim.

ADA Dental Codes and Translation Standards

Clear English descriptions make the claim easier to review. If the clinic can also include Current Dental Terminology (CDT) codes or standard ADA procedure descriptions, a US benefits team will usually find the paperwork easier to understand, because CDT is the ADA’s standard system for dental reporting. If the original records are not in clear English, a professional translation can also help avoid confusion during review.

Financial Coordination: Structuring Multi-Stage Implant Placements

Dental implant treatment often happens in stages rather than during one short visit. The surgical phase usually comes first, followed by a healing period while the implant bonds with the bone, and the final crown or bridge is placed later. According to the ADA, this process can take several months, with osseointegration often taking around three to six months.

That timeline can actually make planning easier. Many patients use the gap between treatment stages to spread costs across more than one tax year, which can make the financial side more manageable. When the treatment schedule and the funding plan are aligned, the overall process is often easier to handle.

Tapping the Rollover Power of HSAs for Multi-Visit Oral Surgery

An HSA gives patients more flexibility here. The IRS allows HSA funds to be used tax-free for qualified medical expenses incurred after the account is opened, and the money does not have to be used within a single year. That gives patients more room to build funds over time and use them when each stage of treatment becomes due.

This approach can work especially well for implant treatment, which often happens in stages. A patient might use HSA funds for scans, grafting, and implant placement in one year, then use rolled-over funds or new contributions for the prosthetic phase on the second visit.

That kind of flexibility matters because these accounts already hold substantial healthcare savings. According to the Devenir HSA Research Report, Americans held nearly $174 billion in HSA assets across 41.7 million active accounts at the end of 2025.

Navigating the Use-It-or-Lose-It FSA Lifecycle Across Financial Years

FSAs need closer timing. For 2026, the IRS health FSA contribution limit is $3,400, and unused funds are generally subject to the use-it-or-lose-it rule unless the employer offers either a carryover or a grace period.

If the plan allows carryover, up to $680 can move into the next year. If it uses a grace period instead, you may have up to two months and 15 days after the plan year ends to use the remaining balance. A plan can offer one of these options, but not both.

For that reason, FSA users need to map treatment dates carefully. A practical approach is to use the current year’s FSA balance for the first surgical trip, then schedule the restorative phase after the next plan year opens. Before booking flights, check your plan documents carefully so you understand the deadline, the carryover rules, and whether your employer offers a grace period instead.

FAQs

Yes, in many cases you can. If the dental treatment in Turkey is a qualified medical expense under IRS rules, is legal where it is performed, and is legal under US rules, HSA funds can generally be used for it or used to reimburse yourself later. According to HealthEquity, overseas HSA card use may also trigger a 1% to 3% foreign conversion fee, which is why many patients prefer to pay directly and reimburse themselves from the HSA afterward.

Usually yes, when the treatment is restorative dental care such as implants, crowns, or surgery that treats disease or restores function. According to the IRS, medical expenses include dental services that diagnose, treat, or affect the structure or function of the body, while cosmetic procedures that only improve appearance do not qualify.

Airfare, hotel upgrades, and tourism costs are separate: the IRS allows transportation primarily for and essential to medical care, and only limited lodging in narrow situations, so a leisure trip wrapped around treatment is not fully HSA-eligible.

It can, but FSAs are more restrictive than HSAs. The expense still has to qualify under US rules, and the plan administrator may ask for itemized records, clear English documentation, and formal approval before reimbursing the claim. Even when the treatment itself is eligible, the card may still be declined during an overseas payment.

It can be safe, but it depends on the clinic, the treatment plan, and the quality of aftercare. The CDC notes that medical tourism carries real risks because standards and oversight can vary from one provider to another. Before moving forward, patients should check the clinic’s licensure, diagnostic process, infection control standards, material traceability, and what support will be available if they need adjustments or if problems develop after they return home.

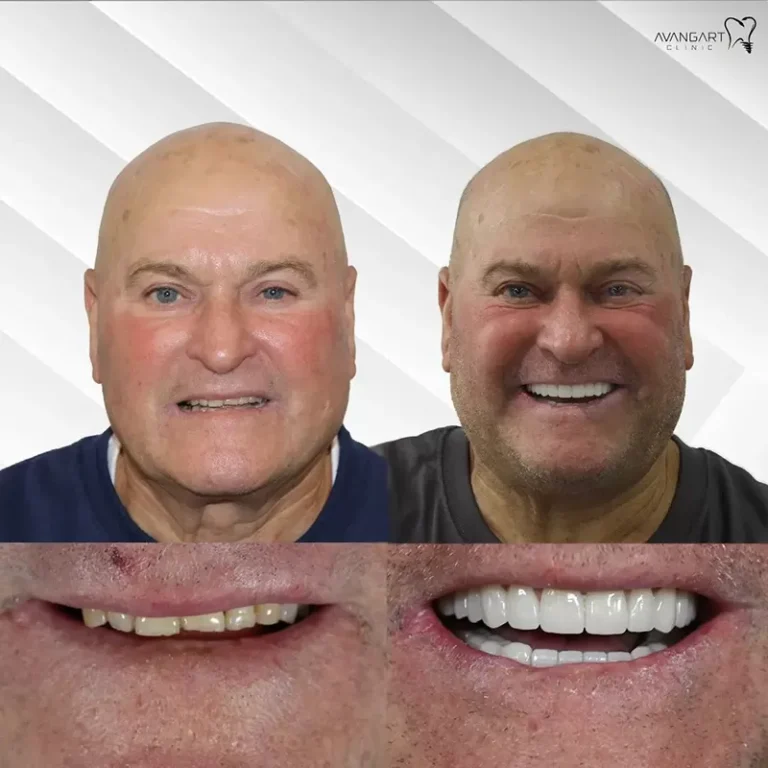

Before and After: Transformative Results with Avangart Clinic

We carry out all our dental treatments with care and strive to give your smile an elegant appearance.